Blog Layout

Property Investment Guest Post By Ed McKnight / Economist at Opes Partners

Ed McKnight • Nov 10, 2019

How to Analyse Whether To Invest In A Suburb – A Working Example

When you invest in a property you are really making an investment in the market the property is located in.

This is similar to the old adage “buy the worst house in the best street”. If you buy an average property in a great market, it is likely you will do well over the long term. However, invest in a great house in a poorly performing market and you are probably going to achieve mediocre returns.

That's why when starting your property investment journey it's essential to take the time to analyse the market, the city and suburb your prospective investment is in. Don't just think about the property alone.

A client recently asked me why we recommended an investment in Cashmere, Christchurch. I thought I would share the response, as it may be a useful case study, showing how to analyse a suburb's property market.

Does the Cashmere property market have strong fundamentals?

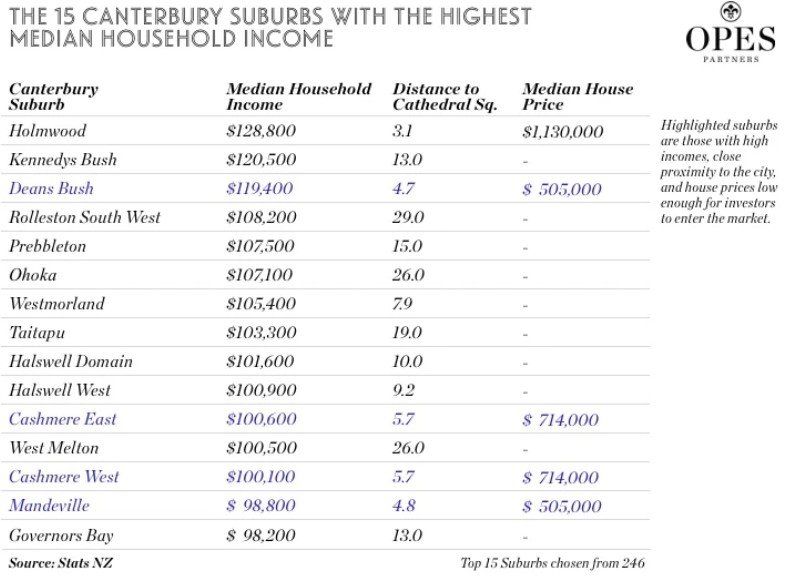

The first place we look to see if a suburb's property market has strong fundamentals is median household income and homeownership stats in the suburb. High household incomes and homeownership are indicators this suburb is an in-demand place to live.

If a suburb is preferred by wealthy people who own properties, this is likely to continue into the future. This demand from people who can afford higher prices suggests property values could continue to increase over time.

Of the 246 Canterbury suburbs investigated, Cashmere East and West rank 11th and 13th on Median Household Income (see below).

The proportion of people living in their own homes in these two suburbs is also much higher than the Christchurch City average. Cashmere's homeownership is between 84-86%, compared with 62-64% for the whole city.

These two stats are positive indicators for Cashmere's long-term property market.

How does Cashmere compare with other suburbs?

The majority of the suburbs that ranked in the top 15 for median household income are also worth investigating as investment options.

In this case, most of the other 15 suburbs are located far away from the central city.

Right now we feel there is a real opportunity to invest in the Christchurch City District. This is because over the next 10 years we expect property prices will benefit from the refreshed CBD, as well as infrastructure investment from Christchurch City Council.

This is supported by KPMG's Magnet City Framework. This report from the UK states Christchurch is among one of the most magnetic second-tier cities in the world (alongside Oklahoma City, Pittsburgh and Tel Aviv).

This means that Christchurch is likely to attract significant population growth in the future (and population growth from young wealth creators).

Of the remaining five suburbs, one (Holmwood) has a prohibitively high entry price for most investors. Although Holmwood has the highest median household income, it also has a median house price of $1,130,000. We feel this means it is not practical for an investor to enter the Holmwood market.

However, for the purpose of this analysis, Mandeville and Deans Bush (both in Riccarton) are worth considering. They also enjoy strong fundamentals, high incomes and close proximity to the city.

Which suburbs achieved the best gains for property owners since the turn of the century?

While historical performance makes no guarantee of future performance, understanding what has happened in the past helps us to think about what could happen in the future.

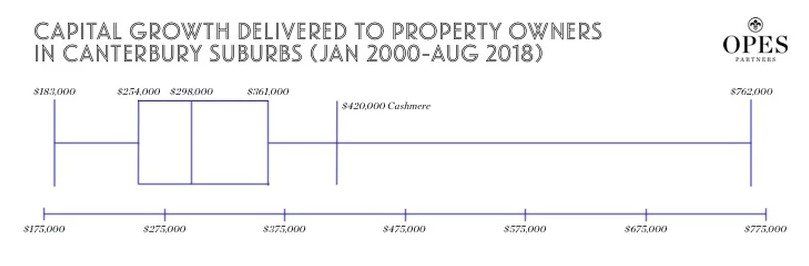

For this analysis, we considered the capital gain achieved within 60 Christchurch suburbs over the last 18.5 years (2000 to mid-2018).

Over that time, Cashmere homeowners received higher capital gains than 87% of property owners in other suburbs, see below. And the suburbs that achieved exceptional capital gain above Cashmere are again the prohibitively expensive suburbs, e.g. Fendalton.

To precisely compare Cashmere to Riccarton: Riccarton came 23rd in the list of suburbs that delivered the highest capital gains to their owners.

Over the last 18.5 years, Cashmere property owners earned $99,000 more in capital gain than Riccarton property owners. This is why, for this client, we had greater confidence in Cashmere, as an investment, over alternatives in Riccarton.

But Cashmere (and Christchurch) property prices are flat. Why would anyone invest in a flat market?

These clients also had concerns about investing in a relatively flat property market.

I believe that if you're not investing in a flat market, you're getting into the market too late. If you buy property when values are already increasing, then another property owner will receive the capital gains you could have earned. The key is to invest in the right area that appears to have strong fundamentals.

This can be seen in historical data. Cashmere was flat from the start of 2000 until the end of 2002. Prices actually decreased and then recovered. Prices then climbed by $289,000 over the next 6 years, before coming back and flattening off for the next four.

Since 2012, the market has slowly climbed and has still generated $124,000 in increased wealth for Cashmere property owners.

If you invested at the start of that flat market in 2000, you still would have achieved gains of $420,000 by backing Cashmere.

It's possible to make good money in a flat market, you just need to hold for the long term so that the market fundamentals have a chance to play out.

Summary

Now, of course, I can't tell you when property prices will increase, or even if property prices will increase.

But what I can say is that when I compare the fundamentals of the Cashmere property market with other suburbs and look at historical performance, Cashmere appears to make a good investment.

Whenever I write an analysis of a suburb or city, I no doubt attract criticism about what I've included, or what I've left out. A recent Stuff article I wrote attracted outrageous comments!

The important thing to me is that when making a property investment decision, rely on data. Rely on facts. Decide what data you think is essential and then conduct an analysis.

And if you need help running these types of analyses, then work with a property coach like Opes or seek advice from a professional, like those at Adair Mortgages.

By Ed McKnight / Economist at Opes Partners

You can save thousands in interest and cut years off your repayments with just a few small changes to your mortgage structure. A lot of people may not realise the total cost of their home. As a very rough guide, a 30 year loan term could cost you twice the amount you originally paid for your home. For example, if you purchased a property for $500,000 with a 20% deposit, that means you have a $400,000 mortgage. Say with a 5.75% interest rate, over 30 years, that would mean a total interest cost of $439,766... making the total cost of your home $939,766! Admittedly the current fixed rates are a lot lower than the above, but history shows 5.75% is a very reasonable rate to work with. Pretty scary to look at those numbers, I know, but this is where I can usually help. A few small changes can make a very big difference. In the above case, if you increased your repayments by just $12 per week, you would save $28,251 in interest. I am sure we can all manage that! Or, if you can manage to pay an extra $100 per week, this saves over $157,000! These simple examples just show that anything you save now can make a huge difference to your financial position. Of course there are other ways that can increase these savings even more, especially if your budget is a bit tight. Loan structure is a big one, as everyone's situation is different. You may be self-employed, so could have an unpredictable income. This may mean locking in an extra $100 per week is unrealistic, so a revolving or offset mortgage may suit you better. An offset loan is a loan that you can link your savings accounts to and any money held in these accounts reduces the portion of your loan that is charged interest. This would mean an interest saving of 5.75% in the above case. Obviously that is much more than you would earn in your everyday savings account. How it works in this case:A $400,000 mortgage with $25,000 savings linked, would mean you are only charged interest on $375,000 of your mortgage. If you managed to leave that $25,000 there for the whole mortgage term, but still paid the standard weekly repayment, you would repay your loan 4 years earlier and save over $95,000. Add that extra $12 per week and it makes your total savings $116,961 and 5 years of repaying a mortgage! Of course, everyone’s situation is different, so I always suggest to get in touch with a good mortgage broker, whether that is me or someone else. A little mortgage advice can go a very long way. These are just examples of how you may benefit from talking to a professional. Also, as your equity grows, we can look at property investment which may help you repay your mortgage even faster. This blog is of course not intended to be personalised financial advice in any way, it is simply showing some examples of how I may be able to help you save with your mortgage. So don’t delay, just get in touch for a chat about your situation. It may save you more than you can imagine, and as I mentioned, my services are completely free to you. All the best for now, thanks for reading. Chad Adair Financial Adviser, specialising in Mortgage Advice. #savings #networth #wealthcreation Adair Mortgages are leading mortgage advisers in Christchurch, Queenstown and Wanaka. Give Chad a call today!

The new season is a great reason to make and keep resolutions. Whether it’s eating well or cleaning out the garage, here are some tips for making and keeping resolutions.

Coming from a property investment background, I know how property can help you repay your mortgage earlier and grow long-term wealth. When I am talking about property investment, I mean long-term investment; Purchasing a property and renting it to a tenant who pays your mortgage for you. Meanwhile, you take the capital growth over time with a hands-off approach. This creates a lower risk profile than anyone trying to speculate or time the market over a shorter term. Most people can understand that property grows in value over time, just look at what your property was worth 5, 10, 20 years ago and compare it to now. However most people also do not understand how to utilise the opportunity, often thinking they cannot afford an investment or simply don’t know where or how to start. This is where getting sound advice from professionals comes into play. Getting the right accountants, property managers, mortgage advisers and even real estate agents, can make the process a whole lot easier and more profitable at the same time. A couple of things that make property investment a good option: Not only is the tenant paying the mortgage on the property, but you might not need to put any of your own savings into the investment either. You can often use the bank's money for 100% of the purchase price (if you have already paid down your own mortgage enough and can afford the debt). This maximises your potential gains and means you can focus on reducing your own personal mortgage (or using your money in more beneficial ways). If you did need to invest some savings for your deposit, and say you have $120,000, you could potentially buy an investment property of $400,000 (or up to $600,000 for a new build due to LVR restrictions of 70% and 80%+). That means this new asset worth $400,000 is increasing in value (not just the $120,000 savings that you initially invested). Say this new property increases at 6% per annum (historically this is reasonable based on REINZ data), that is $24,000 per year on average (and this compounds too). If you invested your $120,000 in shares and returned a massive 15%, that is still only $18,000, for potentially a higher risk investment in shares. This just shows that you may be able to grow wealth with a hands-off approach, that in turn can be used to repay your own mortgage faster, or simply grow your wealth passively through the use of the right professional help and advice. If you want to discuss your options and see how I can help you structure your investment debt for maximum benefit, please get in touch. This is in no way supposed to be financial advice, as everyone's situation is different and should be reviewed in full. These are simply personal views on property investment backed by some market data from REINZ. Chad Adair Financial Adviser, specialising in Mortgage Advice. #taxsaving #mortgagesaving #property #propertyinvestment Adair Mortgages are leading mortgage advisers in Christchurch, Queenstown and Wanaka. Give Chad a call today!

Expert Mortgage Advisers Christchurch, Queenstown & Wanaka

CONTACT US

021 569 602

chad@adairmortgages.co.nz

Christchurch, Queenstown, Wanaka

chad@adairmortgages.co.nz

Christchurch, Queenstown, Wanaka

New Zealand